Many South Africans are facing unfair or illegal debt collection tactics.

South African consumers are struggling to make ends meet and more often than not, they turn to credit and debt when they run out of money long before month-end due to high prices and interest rates. They are unable to pay their debts and now debt collection is becoming a problem.

With the cost of living climbing steadily, more and more South Africans are finding themselves struggling with debt and instead of getting support, many are pushed around by unfair and sometimes illegal debt collection tactics.

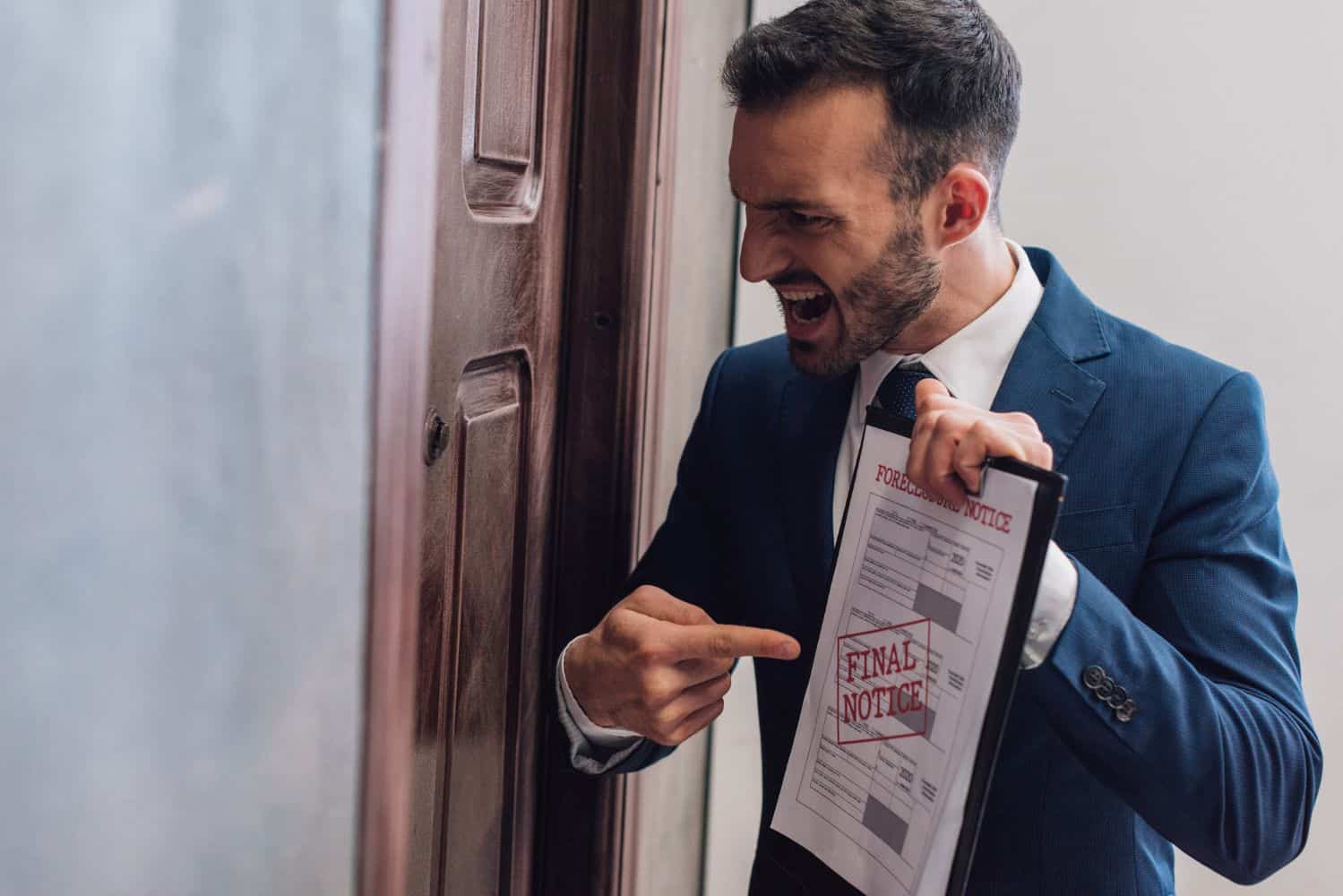

According to Experian, nearly 10 million South Africans are more than three months behind on their debt payments and instead of understanding or help, many face aggressive calls, threats and pressure to pay up, even when the debt should not be collected anymore.

ALSO READ: How to deal with debt collectors

Debt collection harassment

Rynhardt de Lange, director and head of legal at Milaw Legal, says creditor harassment remains a major issue in the debt industry.

One of the most common tricks he sees is how Section 129 notices are misused. “Section 129 notices are meant to open a conversation between the consumer and creditor before any legal action but these days, they are often sent like a final warning meant to scare people instead of helping them figure out a way forward.”

He says consumers often deal with calls late at night, extortion threats and being pushed to pay debts that are too old to collect. South African law protects consumers by limiting when collectors can call, requiring collectors to be registered and banning the collection of old (prescribed) debts.

Unfortunately, De Lange says, these rules are regularly ignored and to make matters worse, financial pressure has been increasing steadily over the past few years.

ALSO READ: Households still credit stressed while their finances weakened

Difficult times cause more disputes about debt collections

“Since 2021 the prime interest rate climbed from 7% to 10.75%, while the cost of essentials such as fuel, food and housing surged sharply. Over the past five years, overall inflation increased by 26.7%, with food prices soaring by around 40%.

“The cost of electricity and household fuels saw the largest jump, increasing by 68.1%. Education expenses also increased significantly, with primary and secondary school fees up by 31.3%. With this kind of financial pressure, it is no surprise that disputes with creditors are increasing.”

However, he says, consumers have the right to stand up for themselves. “In the end, most South Africans are not trying to dodge their debts. They just want a fair chance to get back on track without being bullied.”

ALSO READ: South Africans entering 2025 drowning in debt and without any savings

Remember these rights about debt collections

De Lange shares these five key protections every South African should know when dealing with debt or credit providers:

- 1. Creditors must follow the law before suing you:They have to send you a Section 129 notice and give you 20 days to respond before taking any legal action.

- 2. Harassment is illegal: Collectors cannot call you after hours or on Sundays and they cannot use threats or intimidation. If you feel you are being harassed, report it to the National Credit Regulator (NCR) or the Debt Collectors Council.

- 3. You have the right to negotiate: You can ask for payment plans or apply for debt mediation and creditors are required to seriously consider any reasonable offers you make.

- 4. Old (prescribed) debt is not collectible: If you did not pay a debt or had contact from the creditor for three years or more, you can legally refuse to pay it.

- 5. Collectors must be registered and prove the debt: Always ask debt collectors for their ID and documentation proving you owe the debt. No proof means no payment.

ALSO READ: Watch out! – Some SA banks rip off customers with shady debt collections

Legal protection against illegal debt collections

De Lange says the National Credit Act was designed to protect consumers and make sure lending is fair, affordable and transparent.

“It also set up the National Credit Regulator and National Consumer Tribunal to keep everyone in check. However, too many creditors still ignore these rules and consumers must know they have rights and that the law is on their side.”