We are already inundated with advertising telling us that there are some really special prices heading our way on Black Friday.

Black Friday is coming up on 29 November, but shops are already cashing in on the buying frenzy by offering special prices for the whole month of November. But are these specials really that special and do you really save money?

As the hype around Black Friday creates a frenzy of excitement, most of us wait in anticipation for the annual extravaganza and all its tempting specials. As the marketing machine kicks into gear, advertising creates the desire in many of us to splurge on products we cannot resist buying although we often do not even need them, Steven Amey, head of intermediated distribution at Ashburton Investments, says.

The pull is so strong that, according to Forbes, Black Friday global sales in 2022 reached a staggering $65.3 billion. But what would you see if you could zoom out and look at your Black Friday spending over time compared to what would have happened if you invested that same money?

ALSO READ: Black Friday: will we get proper discounts this year?

Invest rather than spend

“Once you start looking at that picture, many things will become clearer,” Amey says.

“Most of us are emotional beings and we convince ourselves that we deserve to be spoilt. We crave fulfilment and we use our logic to justify these cravings. There is a certain thrill to splashing out.

“However, if we can pull ourselves out of that temptation for a second and look at what we truly owe ourselves, what we can really afford to spend and what we can truly achieve with our hard-earned money, saving and investing becomes appealing.”

Amey says you must ask yourself: “Am I truly saving money by spending on Black Friday specials, or would I be better off saving that same money and placing it in an investment that can grow over time?”

ALSO READ: Spend your money wisely this Black Friday

Before you spend on Black Friday, consider this

Before you decide, Amey says you must consider:

- Are the items you want to buy really cheaper on Black Friday? A report by “Which?” found that 98% of products on sale in the UK during Black Friday 2021 were cheaper or the same price at other times during the year.

- There will always be specials, can I resist the need for instant gratification, especially when there is the added peer pressure of Black Friday?

- Would it not be wiser to save until you can afford to pay cash for something you want or need instead of incurring additional debt? You do not want to regret your purchase due to the additional debt burden a couple of weeks later, only to experience the dreaded buyers’ remorse. You want to enjoy the item well after you bought it, without the pressure of feeling guilty.

- Will you still be enjoying the new TV you bought in 2024 or would the money you could have invested instead put you in a far better place, financially, in 20- or 30-years’ time? Think about your future self, and what you would thank yourself for in the years to come.

Amey says it is also important to understand the true impact of debt before you borrow money to shop on Black Friday.

“In South Africa, according to Eighty20, the middle-class group pays approximately 80% of their net salary to service debt. This debt is loaded with interest rates that far exceed the average salary increase. Therefore, servicing debt with 80% of your salary, at an interest rate that far exceeds your annual salary increase, can only end in disaster.”

ALSO READ: Hey, Big Spender! Black Friday shopper blows R800k in one go…

Example: Mr Freddy Friday, the illustrious feel-good shopper

He says the impact of this debt-seeking behaviour profoundly affects people in retirement, as only 6% of South Africans can afford to retire comfortably. He uses these three special characters to illustrate his point:

- Mr Freddy Friday, the illustrious feel-good shopper

- Mr Debt Interest, the capital destroyer

- Miss Compound Interest, the joyous wealth creator

“Mr Freddy Friday loves to shop, especially on Black Friday. Freddy earns a salary of R600 000 per year and his average annual increase is 5%. Freddy has been on shopping sprees for years and has accumulated debt amounting to R480 000 that comes with the well-known capital destroyer, Mr Debt Interest, who charges a hefty interest rate of 22% per year for his services of lending money to Mr Freddy Friday.

“But Freddy’s consumption behaviour has caught up with him. To get out of this hole of debt, he agreed to pay back his debt over 15 years with repayments of R9 148 per month. The debt that started out at less than a half a million rand will amount to a total of R1.6 million over the 15 years.

“Think of that for a moment: Mr Freddy Friday’s debt has cost him more than three times the actual purchase price of his goods, due to the interest charged by capital destroyer, Mr Debt Interest. Mr Freddy Friday would have spent 70% of the R1.6 million, a shocking total of R1.1 million, on interest alone over the 15-year repayment period.”

ALSO READ: Up your savings: the secret of compound interest and the rule of 72

Here comes Miss Compound Interest

Now Amey offers an alternative outcome, similar to a choose-your-own-adventure and introduces Miss Compound Interest, who talks to Freddy about his exorbitant buying habits.

“She convinces Freddy to only buy what he really needs and a little of what he likes and to save and invest the rest. Freddy decides to give this a try and instead of spending on Black Friday, he puts the money aside for investment.

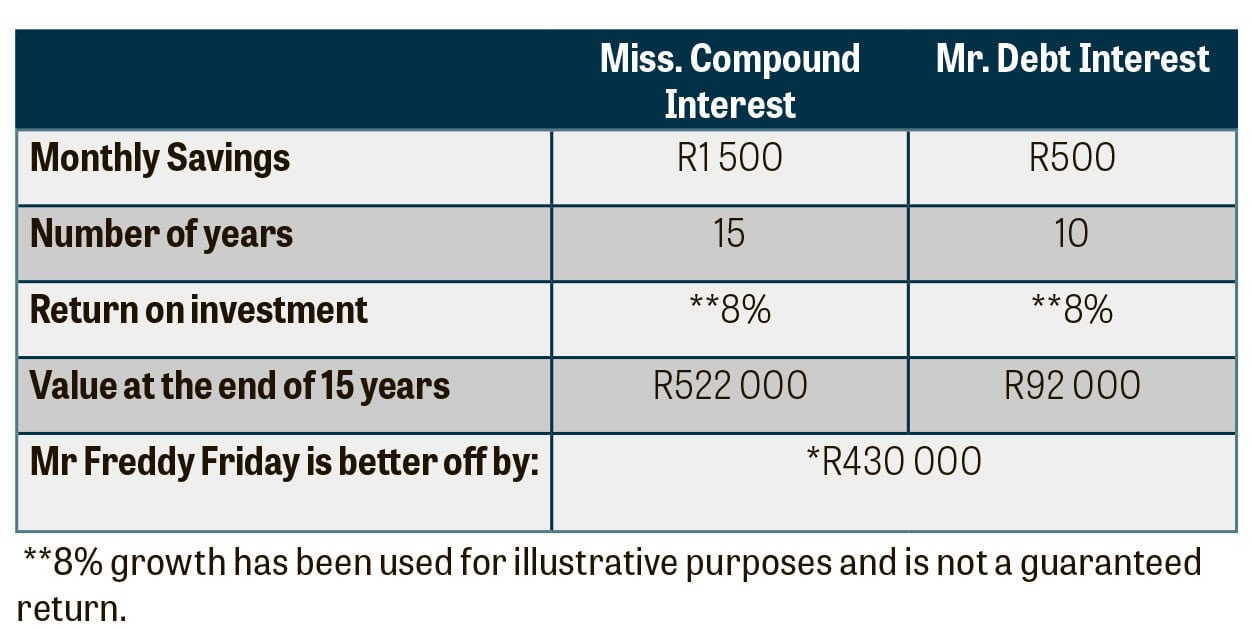

“Where he previously saved R500 per month towards his retirement, he can now save R1 500 five years earlier. If we assume Freddy’s investment was placed in a unit trust, which generates a return of 8%, excluding tax per year, Freddy will undoubtedly look back in 15 years’ time on thank his lucky stars that he could make R522 000.

“This was only possible because he acted on the guidance of Miss Compound Interest and benefited from saving more, saving earlier and enjoying the benefits of compound growth over the period.”

ALSO READ: What to consider when deciding to invest locally or offshore

How much you can save by not spending on Black Friday

This is how things could turn out if you make good choices, Amey says, with this table showing the impact of investing compared to spending:

“Let’s all take a moment to think, before the debt train runs away with us. Realise that debt interest is a capital destroyer and you could live very well without accumulating a lot of stuff that will not be worth much to you later in your life.

“Think for yourself and do not get swept up in the hype of Black Friday. Rather make friends with Miss Compound Interest earlier in your life and end up with accumulated wealth when you are older that will enable you to enjoy life, having less financial stress in retirement.”