After the minister tried to push though VAT increases in his first two budget attempts, Budget 3.0 will still affect citizens’ pockets.

It was indeed third time lucky for Minister of Finance Enoch Godongwana when he delivered Budget 3.0 in parliament on Wednesday afternoon with the blessing of all the parties in the government of national unity.

Frank Blackmore, lead economist at KPMG, says probably the most impressive thing about Budget 3.0 was that we now have a budget at all, although the contents were a bit underwhelming.

“There were many questions about what we are going to do with the R75 billion deficit over the medium-term period with no VAT increase. That was answered by this budget in the form of:

- some increases in the fuel levy of 15-16 cents per litre;

- an increase in borrowing with debt going up to 77.4% of gross domestic product (GDP), 1.2% more than in Budget 2.0;

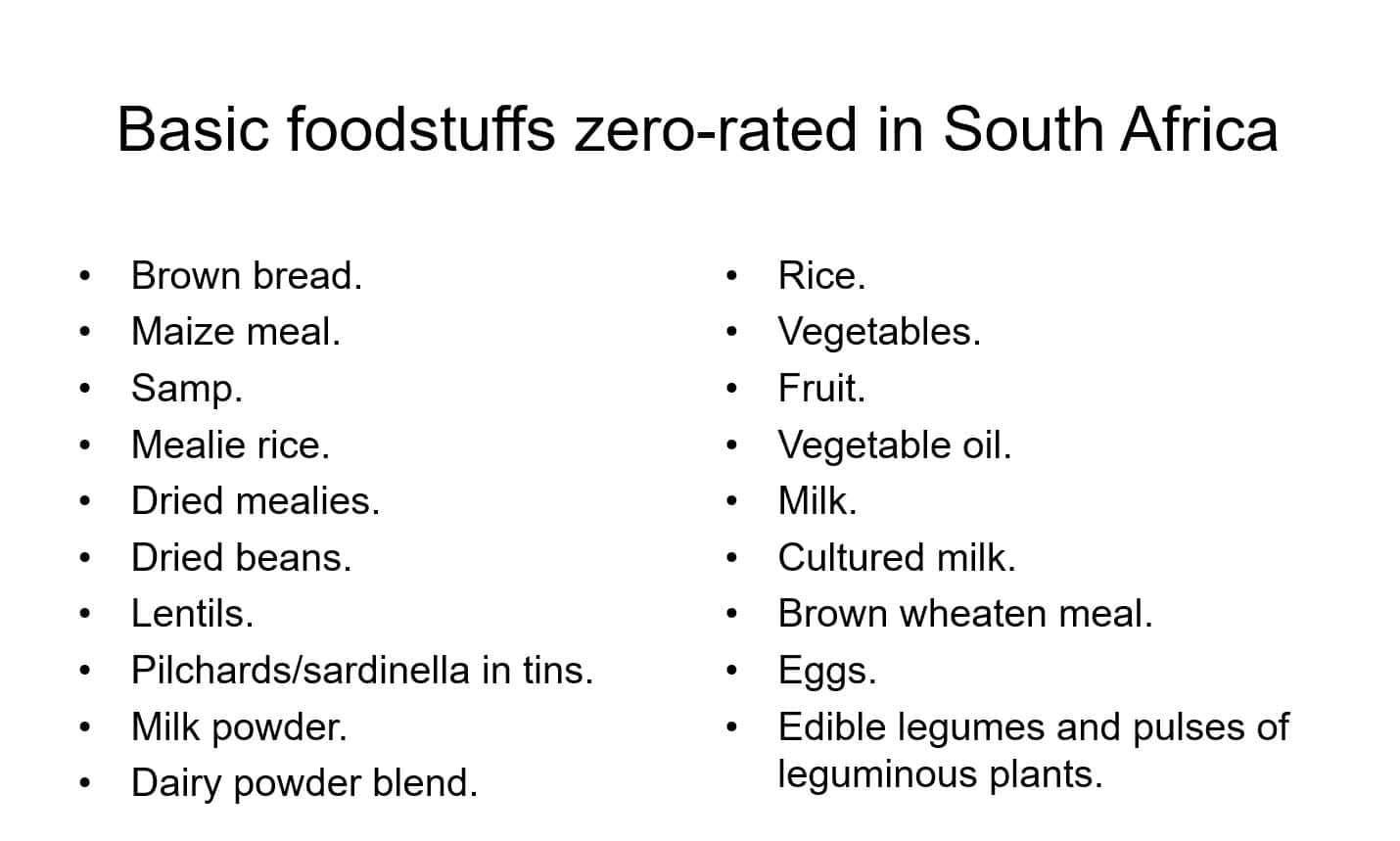

- no expansion of the zero-rated food basket;

- reduced expenditure over the Medium Term Expenditure Framework (MTEF) period;

- the budgets of frontline services such as health and education growing, but by less than the previous budgetary amounts;

- some additional investment will go to Sars to switch those assets in order to collect more revenue.

ALSO READ: Budget 3.0: not austerity budget, but a redistributive budget

Not much thought about issues confronting SA

Blackmore says it seemed that the budget was focused on these points without dealing with the issues confronting South Africa at this point. “There were reductions in a lot of areas that were obviously necessary due to lower revenues, except for the public sector wage bill and debt deficit which are increasing.”

He says the negatives in Budget 3.0 are:

- the increased debt and deficit taking more resources away from frontline services and economic growth initiatives, such as the social wage

- the reduction in the growth of non-interest expenditure

- no real increase in spending to grow the economy

- a mention that new tax proposals will come in for 2026 to cover an additional R20 billion gap for the full cost for that period.

He did not find much on the positive side but says the public private partnerships and continuing structural reforms, as well as Operation Vulindlela Phase 2 are positive, but are nowhere near large enough to make a meaningful difference at this point to the growth outlook.

ALSO READ: Godongwana cuts government spending to offset VAT shortfall

Budget 3.0 a more realistic picture of SA’s macroeconomic outlook

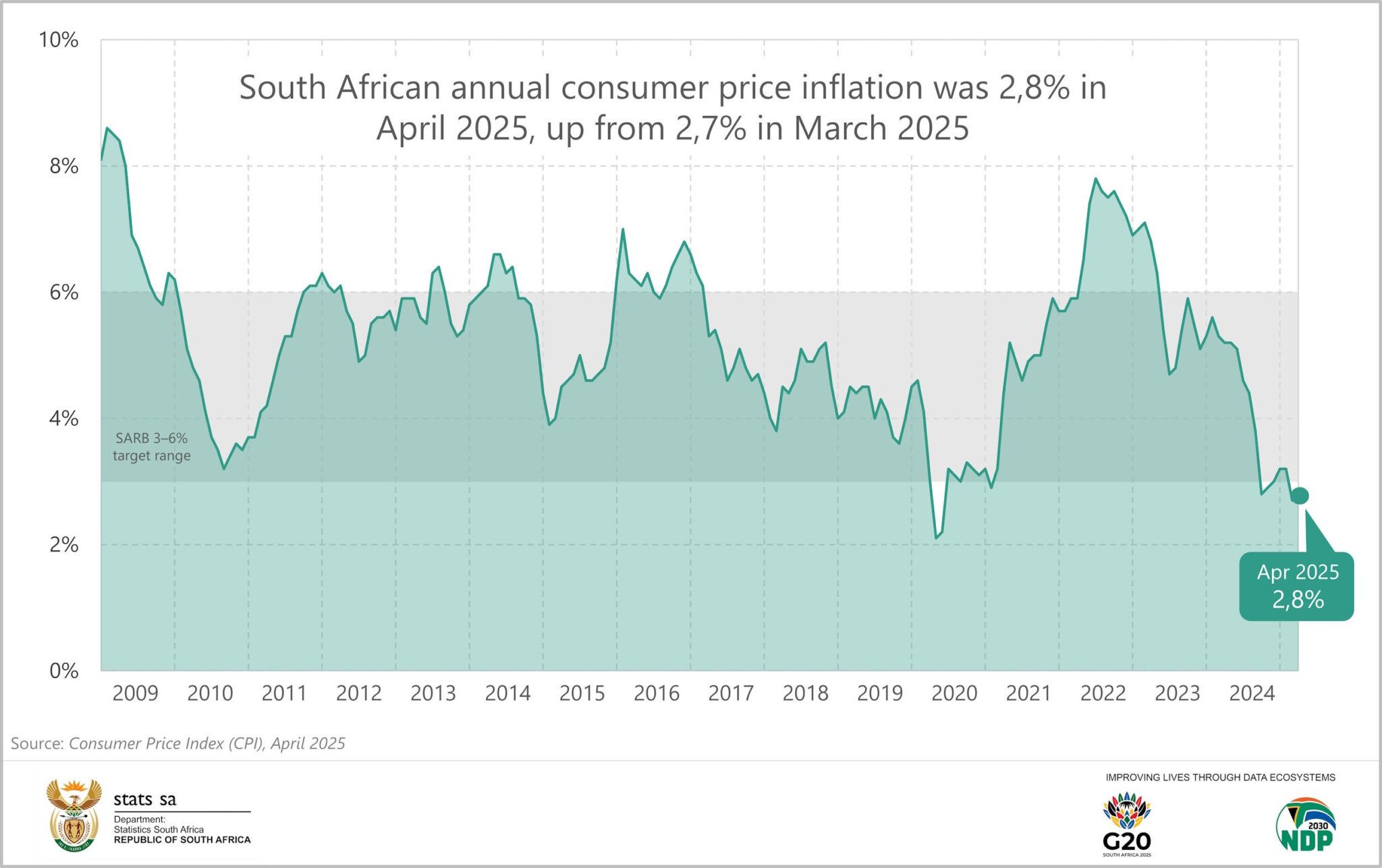

Jee-A van der Linde, senior economist at Oxford Economics Africa, says Treasury’s downwardly revised GDP growth projections and higher debt-to-GDP ratios paint a more realistic picture of South Africa’s macroeconomic outlook.

He says it is a positive takeaway that gross loan debt projections have not increased since March and Treasury still expects debt levels to stabilise, although at a higher level. Gross loan debt is expected to increase from R5.69 trillion in 2024/25 to R6.82 trillion in 2027/28.

“Meanwhile, debt-service cost projections were lowered by R1.8 billion over the MTEF period compared to the March 2025 Budget. South Africa’s debt service costs remain alarmingly high at R1.3 trillion over the MTEF and we expect it to continue rising rapidly over the forecast period.

“South Africa’s deteriorating debt-to-GDP ratio remains a concern and we continue to maintain that gross government debt will reach 80% of GDP in the near term. The sustainability of South Africa’s fiscal outlook hinges on economic growth accelerating in the near term, as fiscal consolidation will prove challenging amid elevated spending pressures.”

Was it third time lucky for Godongwana? Van der Linde says Budget 3.0 is more sensible and depicts a stark picture of South Africa’s finances. “Markets will welcome Treasury’s commitment to fiscal consolidation.

“While not of its own making, Treasury’s credibility has been unduly dented as a result of the budget wrangling. Political parties have been climbing over each other trying to claim credit for Treasury reversing course on the tax proposals that scuppered the first and second budget attempts.”

ALSO READ: Budget 3.0: Opposition parties clash over impact on poor

Very high execution risk

Patrick Buthelezi, economist at Sanlam Investments, says the execution risk for the budget remains very high as many spending pressures require funding, such as closing the gap created by a freeze on PEPFAR support, political party funding leading up to the local government elections and national social dialogue.

“Given the projected economic growth outlook, the pressure on the fiscus can be expected to continue. The finance minister hinted that revenue-raising measures might be introduced in the 2026 budget. The GNU needs to reach consensus on viable revenue-raising proposals, including expenditure cuts.”

Tertia Jacobs, treasury economist and fixed income specialist at Investec, says for her a key takeaway is that the GNU and Treasury continue to stick to fiscal consolidation.

“Any new increases in spending must be financed by higher tax increases and the new spending increases are allocated between infrastructure and frontline services as well as Sars getting a bit more money because they will become more important in widening the tax base in coming years.

“All in all, the budget is probably as good as we can get in the context of sluggish growth, but these are indications that the GNU and the ANC are willing to work together.

ALSO READ: Budget 3.0: Alcohol and cigarette prices will increase — here’s by how much

Commitment to stabilising government debt

Dr Elna Moolman, head of South Africa macroeconomic research at the Standard Bank Group, says in line with their long-standing expectation, all three budgets this year remained committed to stabilising government’s debt-GDP ratio.

“The negative revenue impact of backtracking on the VAT increases as well as the weaker economic growth trajectory is counteracted, as we expected, by a combination of revenue and spending adjustments.

“The confirmation of government’s commitment to fiscal consolidation, with the debt-GDP ratio peaking this year and bond issuance kept unchanged, should provide some reassurance to financial markets, as we expected.

“The macroeconomic policy reviews and fiscal reforms, alongside ongoing traction with Operation Vulindlela’s growth-supportive reforms, also underpin likely fiscal and growth improvements in the medium term.

“However, entrenched investor concerns about adverse fiscal and growth risks will not be negated and notwithstanding the imminent peak in the debt-GDP ratio and unchanged nominal debt trajectory, investors will emphasise yet another increase in the debt-GDP trajectory that will limit the potential positive financial market impact from any positive fiscal developments.”