S&P affirmed SA’s BB- credit rating but changed the outlook from stable to positive and expects gross government debt to reach 80% of GDP.

Rating agency S&P’s rating outlook for South Africa announced on Friday follows Fitch’s more positive rating just before the Mid-Term Budget Policy Statement at the end of October. Both improved outlooks were the result of more policy certainty in the country.

Jee-A van der Linde, senior economist at Oxford Economics Africa, says the risks to the rating agency’s fairly conservative growth forecasts are tilted to the upside, with Standard & Poor (S&P) noting that private sector reform under the new government could bolster economic prospects.

S&P’s latest rating actions follow Fitch’s rating affirmation which affirmed South Africa’s BB- credit rating with a stable outlook. Moody’s Investors Service has not recently issued an update on its Ba2 sovereign credit rating with a stable outlook.

Van der Linde says S&P’s positive outlook change is thanks to a more stable political environment and reflects the possibility of stronger economic growth than anticipated, as well as the stabilising of government debt, provided the new government can expedite economic reforms while resolving concerns pertaining to infrastructure and the fiscus.

ALSO READ: ‘It’s like deciding whether SA is in C-Max or medium prison’ – economist on SA’s Fitch rating

S&P forecast for real GDP growth

“S&P forecasts real GDP [gross domestic product] growth of 1.4% per year from 2025 to 2027 and we forecast 1.7% over the same period, but the agency noted that planned acceleration of economic reforms might lead to a stronger economic pick-up.”

While S&P forecasts gross government debt levels to reach 80% of GDP by 2027, S&P anticipates greater fiscal policy predictability regarding efforts to achieve primary budget surpluses and fiscal consolidation.

However, Van der Linde says, spending on wages and social services, as well as transfers to state-owned enterprises (SOEs), remains a salient risk.

“We argue that there has not been sufficient evidence suggesting that South Africa’s current debt trajectory will flatten. Consequently, we still expect government debt to reach 80% of GDP over the medium term.”

ALSO READ: MTBPS: No SOE bailouts, early retirement for 30 000 public servants

S&P forecast for SOE bailouts

S&P lowered its forecasts for off-budget spending for SOEs compared to their previous review. The agency does not believe the government will provide support similar to the Eskom debt relief package to other SOEs, such as Transnet.

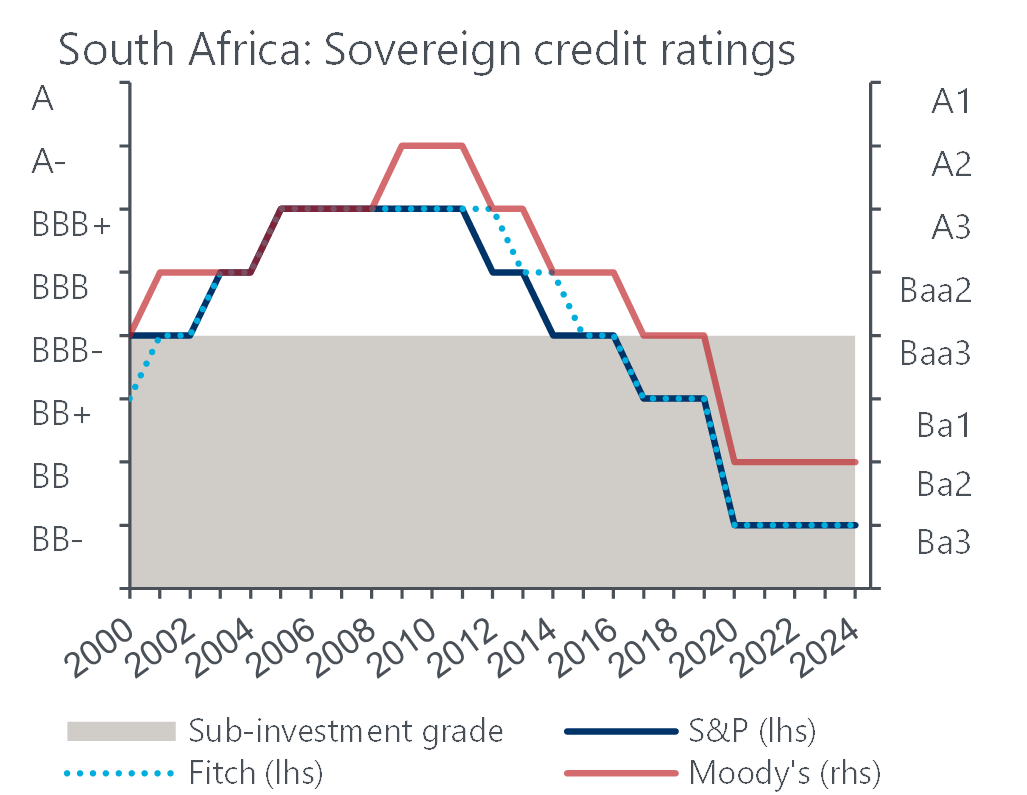

S&P gives South Africa the benefit of the doubt with rating affirmation and a positive outlook as this graph demonstrates:

Source: Fitch, S&P, Moody’s

Van der Linde says Fitch’s September rating assessment was sensible and S&P’s mildly upbeat outlook is also warranted given the decline in short-term policy uncertainty and South Africa’s improved economic outlook with the formation of the Government of National Unity (GNU).

ALSO READ: MTBPS: Not a rosy fiscal picture with disappointing fiscal slippage

Risks to growth outlook largely balanced

“We believe that risks to the growth outlook are largely balanced, with upside surprises now worth mentioning for the first time in years. Moreover, S&P’s positive outlook change also aligns with our view that although the 2024 Medium-Term Budget Policy Statement depicted fiscal slippage, nuances matter and the updated official forecasts present a more realistic picture.”

He says in the immediate term, accelerated economic reform momentum, in collaboration with the private sector, remains vital from an economic growth and foreign investment perspective.

“The government’s pro-growth mid-year budget is encouraging and rating agencies will welcome Treasury’s commitment to fiscal consolidation. These factors, together with a more stable political environment and South Africa’s credit strengths consisting of monetary flexibility, a freely floating exchange rate, deep financial markets and favourable debt structure, imply an improved outlook. However, we believe it is still too early for credit rating upgrades.”